If speaking with the living doesn’t do it, then perhaps conversing with the dead does. Another potential use case of photorealistic avatars within high fidelity immersion is digital “immortality” or reconnecting with deceased family members and friends. Such a topic has been occasionally floated ever since VR came into public consciousness but has never been able to be pulled off given the lack of tech. Now two key technologies are coinciding to make this a possibility – realistic 3D avatar and speech AI like GPT3. It is not hard to imagine that photorealistic avatars combined with a language processing algorithm like openai’s GPT-3 (fed with the right speech text) could generate a realistic VR chatbot of anyone famous or even a deceased loved one. If such potential is realized, it could be the catalyst to convert the non-gamer masses to VR/AR.

There has been no shortage of VR news of late – Meta announced Quest Pro; Bytedance launched Pico 4, pricing it to compete with Quest 2; Sony is expecting to launch 2 million PSVR2 units on 22 Feb 2023; Apple is reportedly developing three headsets to be announced in 2023 (although Apple VR rumors have been around since 2014); On the AR front, Microsoft’s Hololens and Magic Leap have also seen new releases this year.

The most important question in everybody’s mind is whether VR/AR will prove to be the next leap in human-computer interaction since mobile, or will it be history’s biggest nothing-burger. Experts and pundits across the web are on a wide spectrum on this topic. However, data suggests that the future remains promising for the VR/AR market.

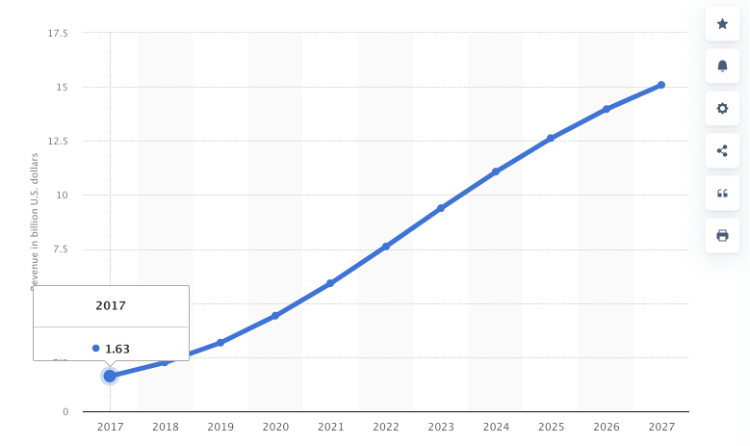

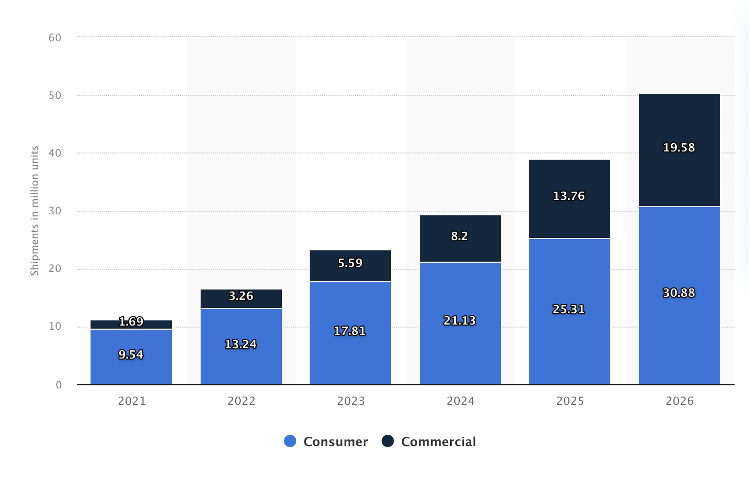

According to statista.com, the trend of VR B2C hardware market is firmly up in the past 5 years, growing 460% from $1.63B in 2017 to $7.6B in 2022. This number is projected to double, increasing to $15.1B in another 5 years. Overall units of headset sales to both consumer and enterprise customers are projected to increase by 300% in 2026, targeting 50.5 million units.

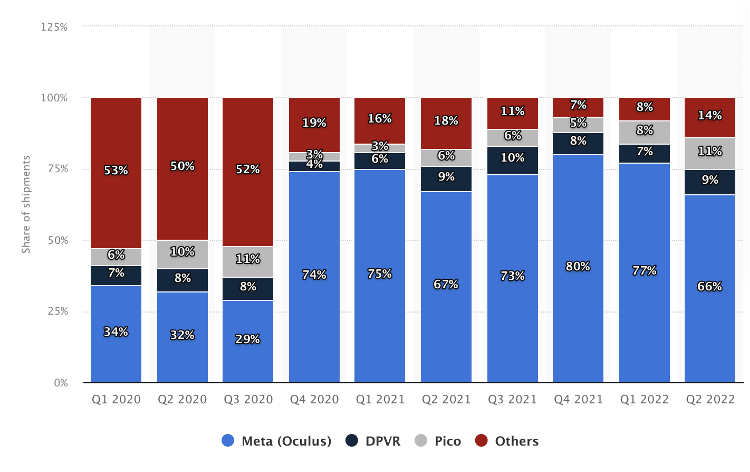

According to a June 2022 report by IDC, Meta has dominated the VR headset market (while burning oodles of cash), capturing 90% of the market with its Quest 2 device in 1Q22. Looking at Steam’s estimation, 64.4% of Steam players are using an Oculus device, with Quest 2 taking a whopping 41.4%. In absolute terms, Quest 2 seems to have sold roughly 15 million units so far. The one thing that is clear, is that Meta is firmly in the pole position by headset sales. However, it took Meta $36B since 2019 to get here and plans to spend another $100B in the next few years. Investors are asking – will this be worth it?

Some investors could see the prudence of such a bet to avoid the Innovator’s Dilemma, but balk at the price taken. Brad Gerstner wrote such an open letter to Zuck. It’s more about the bet sizing rather than the bet itself. “While Meta has been taking a lot of flak lately for its new strategy, I think the problems are driven less by overarching strategy and more by executional nuances… There’s a high likelihood that, once the technology is compact enough, perhaps in five to 10 years, VR/augmented reality (AR) glasses will regularly replace or augment smartphones and laptops depending on the use case. That’s probably why it’s no secret that Apple is working on its own device.” says Sean MacPhedran, senior director of innovation at SCS agency.

Progression of VR technologies

So, what is exactly spent on VR and AR development? What sort of technology goes into a VR headset? And how has technology progressed throughout the years?

According to Meta, the key VR challenges to tackle before the visual Turing Test can be passed are variable focal depth (aka varifocal), optical distortion, retinal resolution, and HDR.

- Varifocal: the ability to focus on different depths of a virtual scene, from near to far

- Optical distortion: solve for lens distortion when light passes through

- Retinal resolution: having enough resolution in the display to meet or exceed the resolving power of the human eye. The target being retina resolution of 60 pixels per degree, allowing for 20/20 vision

- HDR: also known as high dynamic range, describes the range of darkness and brightness that we experience in the real world (which almost no display today can properly emulate). Think about looking at fireworks at night

Here are the few key components that go into a VR headset, required to achieve ever higher quality of immersive experience.

- Processor (for standalone devices) to render images. If the headset is tethered it would require a base machine such as console, PC, etc. to render images. Otherwise, a stand-alone machine like Quest 2 and Pico 4 would require just an integrated mobile chip. Currently Qualcomm is the de facto chip maker for standalone VR headsets with their Snapdragon XR series.

- Lenses and screen tech to project the rendered images. VR uses stereoscopic lenses placed between the screen and the eyes to simulate the human’s binocular vision and creates a 3D view.

- Motion sensors to track users’ position within virtual reality. Currently the key tech is the so-called Inside-Out Tracking System which uses cameras from the headset to track space around the users. Meta’s new Quest Pro even has Inside-Out Tracking on each controller

- Controllers and haptics to navigate within virtual reality. This includes moving the user, changing views and interacting with objects in the virtual environment

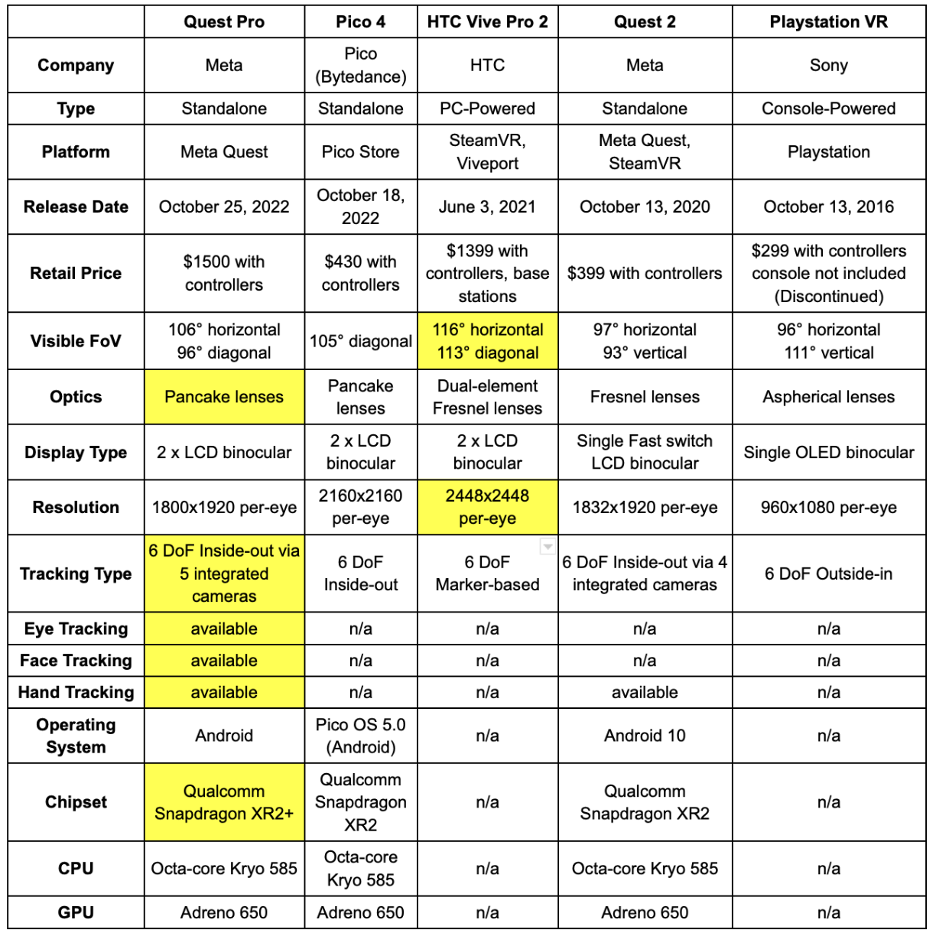

The development of these key technologies will dictate the quality of immersion, price and size of device, which will in turn dictate market appetite. Here are the developments on recent popular devices. We compare Quest Pro, Pico 4, HTC Vive Pro 2, Quest 2 and Playstation VR as these are the notable names in the past 5 years. Honorable mentions such as Valve Index, HP Reverb G2 and Varjo Aero are also popular devices among VR enthusiasts but not included in this comparison.

While Meta is focused on standalone headsets, and clearly that seems to have hit a certain product market fit if you look at Quest 2 overall market share. It is not without issues and the key of which will be battery life. Quest Pro (also a standalone device) has roughly half the battery life of Quest 2 as it jams in ever more sensors and processing power to improve on image quality. And even then, tethered-devices which are able to connect to a PC rig with the latest graphic card will likely still beat standalone devices in terms of image quality.

The next high profile tethered device will be PSVR2 launching Feb 2023. The key thing to watch for is specifically the penetration of Sony’s PSVR2. This much awaited update to the original 2016 PSVR will show us if there is any pent-up demand for VR. Will the PSVR2 sales unit surpass the original PSVR? Will it surpass Quest 2? Is there a future for tethered VR devices?

// Source: steamdb.info

Games

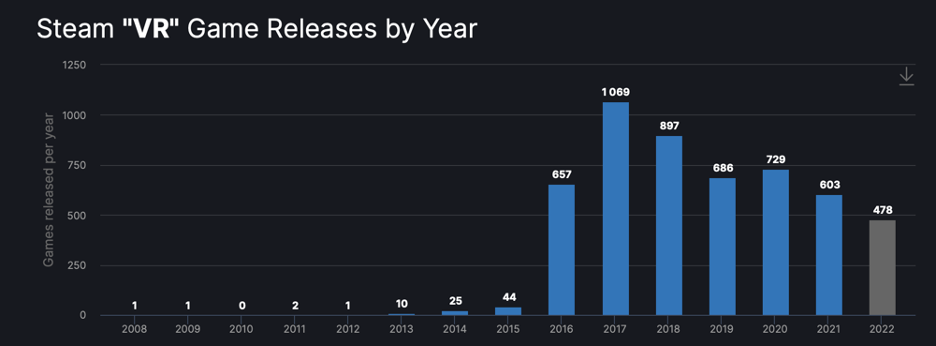

VR games releases exploded in 2016 very much in anticipation of the launch of Oculus Rift Playstation VR and HTC Vive in the same year. Hits such as Arizona Sunshine, No Man’s Sky, VR Chat, and Skyrim VR all launched between 2016 – 2018 and have been updated continuously well into 2022. On the other hand, we see that new VR game releases have been slowing down since the initial 2016 hype. Perhaps that’s what the market can accommodate at the moment and also perhaps studios might still need some convincing. Estonia’s CM Games decided to roll the dice on VR despite management’s initial instinct to avoid it, making Into The Radius which made over $1M in 2021.

Prior to 2016, VR experiences have extremely short gameplay such as ustwo’s Land’s End, which lasts for roughly an hour (but has been in development for more than 16 months). Admittedly VR games in the early days are passion projects by pioneering studios looking to push the boundaries of art and technology. Given that Land’s End was a Samsung Gear VR exclusive, that’s likely where the funding for such a project came from.

And that has been the main problem to solve for when VR has no consumer reach – convincing developers to create content for a medium that has an unknown future. Luckily 2016/2017 was an era of massive VR hype, when multiple VR headsets came out – Samsung Gear in 2015, Oculus Rift in 2016, Playstation VR in 2016, HTC Vive in 2016 all while rallying around a common VR game platform – SteamVR (beta released in 2014). While each headset has their own platform such as HTC’s Viveport and Meta’s Quest store, SteamVR is the neutral VR platform for most players, and developers have a go-to platform without the worry of market fragmentation. Of course, there are still quite a few platform exclusives especially for Quest and PSVR to introduce a degree of product differentiation.

// Source: Google

Fast forward to 2022, the business for VR games is starting to flesh out alongside acquisition activity – Meta has acquired 9 VR studios since 2019 including maker of Beat Saber and Ironman VR while Embracer has acquired Vertigo Games in 2020, maker of Arizona Sunshine. Meta’s recent report about its VR game sales highlighted a few of these developments. Of course, these numbers are still a fraction of the overall PC/Console market, but it is trending in the right direction.

- Meta Quest store has earned $1.5B in revenue on games and apps since May 2019

- Blade & Sorcery: Nomad reached $1M in revenue in two days

- Zenith: The Last City and Resident Evil 4 made $1M and $2M respectively in under 24 hours

- BONELAB earned $1M in less than an hour

- The Walking Dead: Saints & Sinners has brought in over $50M in revenue since October 2020

Apps

Outside of the traditional gaming experience, users are also exploring different use cases on VR. Social and fitness are the two main examples. VRChat and Rec Room are the two leaders in VR social where VRChat can be seen constantly topping SteamVR DAU.

Rec Room also mentioned they have tripled their VR MAU from 1M in 2021 to 3M (peak) in 2022. This recent spotlight by Naavik also highlights Rec Room’s new updates and meteoric rise. Unfortunately, Meta’s flagship “metaverse” app, Horizon World, is still very much a work in progress. It’ll be interesting to see if Meta decides to continue with Horizon World or maybe buy out Rec Room.

Fitness on VR is also another popular use case, with games like Supernatural, a subscription-based workout platform, Beat Saber and Thrill of the Fight etc., all providing a sweat in the comfort of home. This is growing closer to the home fitness market that Peloton and Mirror.co (now Lululemon Studio) is fighting over. Arguably Fitness VR could also be a winner here if the entire home fitness market grows.

So far, we’ve covered mainly the consumer aspects of VR and nothing about professional applications or even AR, we can save that for a separate article. However, it seems that consumer VR should be the major driver in the entire VR/AR market. Microsoft is reportedly scrapping plans for Hololens 3 while focusing on a collaboration on consumer XR with Samsung. The Apple rumor mill of upcoming XR devices in 2023, PSVR2 Feb 2023 launch and Meta’s 2023 Quest 3 are all signals that consumer VR tech (and marketing budget) will be chugging along in the coming years.

Next Phase of XR Adoption

In terms of the future of VR games / apps, we can expect games to be ever more immersive as the graphics get increasingly better with devices and game engines improvement. It will be exciting to see the first VR game made with Unreal Engine 5. Also new VR devices are incorporating mixed reality view which utilizes passthrough cameras, essentially turning it into a AR/XR device. This mode allows users to view physical surroundings while mixing in virtual objects, opening up mixed reality use cases such as digital tabletop games, workstation enhancements, physical collaborations and augmented meetings.

However, the next leap in VR adoption could come from something entirely different – photorealistic avatars. Outside of games, fitness and social, the biggest potential could be communication, either with the living or the dead. As Meta’s photorealistic VR avatar reached another milestone, producing the avatar just with a phone camera, one has to wonder about the chances of photorealistic avatars improving remote work and conference calls. If the experience is indeed a material change when compared to the standard Zoom call, then the ongoing remote-first work trend could push VR adoption higher.