Looking at recent developments on the software front, there are many reasons to be optimistic. Here’s a refresher on some of the announcements from the past 12 months:

- October 2021: Meta (still known as Facebook at the time) teased Polar, a lightweight mobile app for AR creation that leverages the company’s Spark AR platform.

- November 2021: Niantic opened Lightship, the foundation for all of Niantic’s products, to developers globally.

- March 2022: Snap launched Custom Landmarkers, which lets creators produce geospatially anchored AR content.

- April 2022: Snap launched Lens Cloud, a suite of backend services that allows developers to build dynamic, multiplayer experiences.

- June 2022: Apple unveiled a series of improvements coming to the ARKit toolkit across motion capture, camera access, and new “location anchors” for outdoors navigation.

- July 2022: Snap announced Snapchat for Web, a Snapchat+ exclusive that will bring the company’s signature Lenses to millions of new screens.

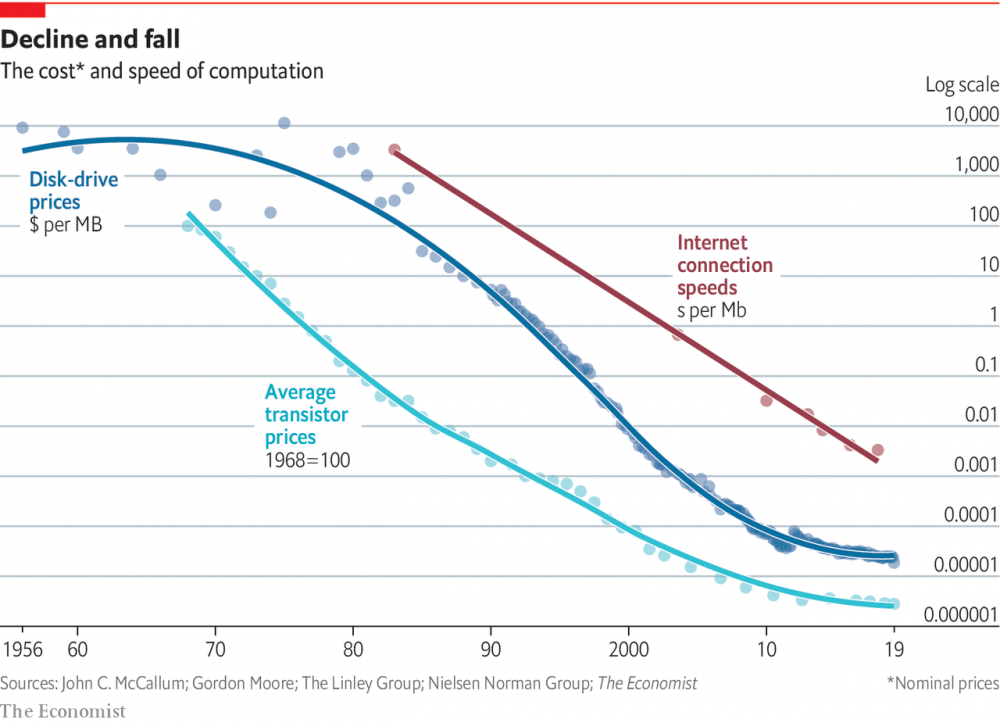

The picture is clear: from one product release to the next, creators and developers are getting access to increasingly advanced AR tools. These platforms provide them with a variety of technology blocks that include everything from face detection to mesh 3D to plane tracking to particle effects. In particular, visual positioning, which lets users place persistent virtual objects in specific locations, has seen multiple breakthroughs that are paving the way for ever-larger and more social experiences. All this is dramatically lowering past barriers to entry and enabling experimentation across all use cases and on all kinds of objects — from faces to products and from landmarks to scenes.

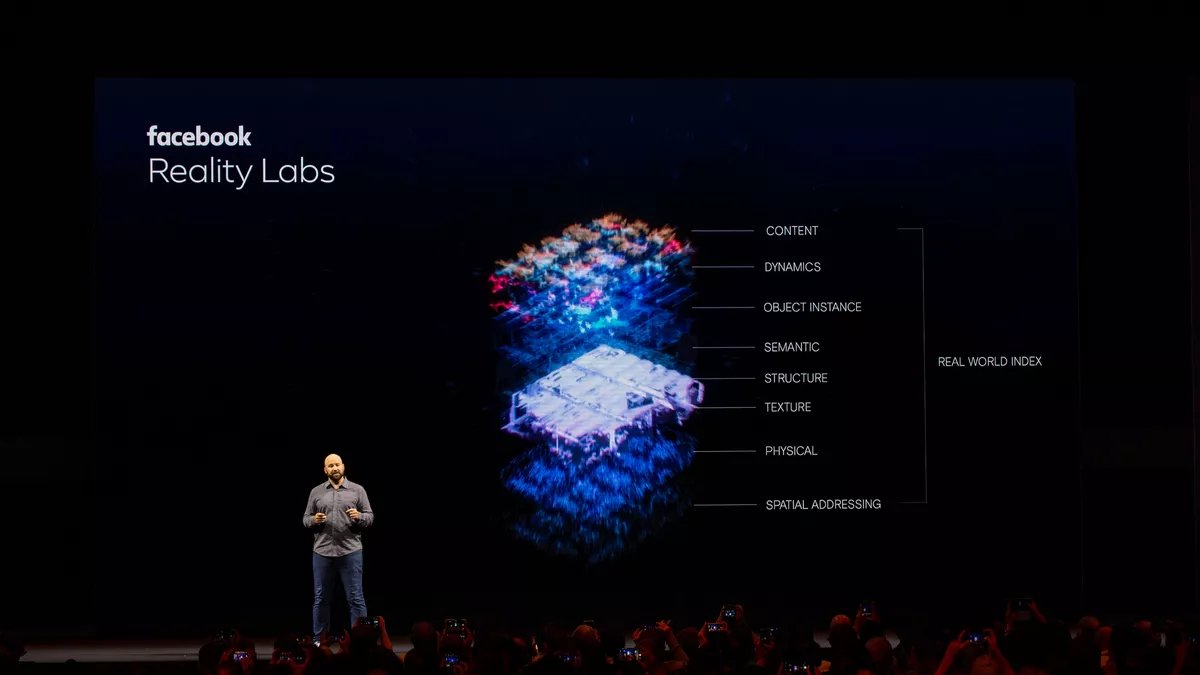

While it’s easy to marvel at the current pace of innovation, it’s all the result of years of patient innovation. Apple’s ARKit and Snap’s Lens Studio both launched in 2017; Google’s ARCore is a continuation of the Tango platform, which launched in 2014 and was discontinued in 2018. Niantic’s Lightship was first introduced in 2018 as the Niantic Real World Platform, while Facebook’s creative platform Spark launched in 2019. Over the years, all these players have not only increased the range of their capabilities, but also made them more accessible through a mix of funding and education.

This process was also bolstered through active M&A. Niantic alone has acquired no less than seven AR-focused startups, including: Escher Reality, a startup developing technology for persistent multiplayer experiences; Matrix Mill, which specialized in 3D occlusion effects; 6D.ai, a spatial mapping company; and 8th Wall, a WebAR development platform. In 2020, Facebook acquired Scape, a company that built 3D maps from ordinary 2D content, while game engine giant Unity acquired RestAR for high-res 3D. (Note that we’re only mentioning software-related acquisitions here, the complete list including hardware would be much longer!) We expect more such moves in the coming months as competitors aim to fill gaps in their respective stacks.

To draw developers in, each player has been leaning on its set of own strengths.

- In Snapchat, Snap has one of the most popular social apps and a notorious Trojan horse for AR: as of April 2022, over 250,000 developers on the app had published a total of 2.5 million Lenses, which had been viewed over 3.5 trillion times in aggregate. Given Snapchat’s demographics, most of this consumption notably comes from younger users: according to Snap, “Gen Z / Millennials are both 71% more likely to use AR all the time vs. older generations.”

- Apple has the reach and authority of iOS, as well as decades of know-how in maximizing the potential of its hardware. The addition of LiDAR technology to the “Pro” versions of the iPad and iPhone further increased the company’s lead on that front by bringing improved depth-sensing capabilities to these devices.

- Google can leverage services like Google Translate, Lens, Search, and Maps to enable real-time translation, browsing, shopping, and navigation.

- Alongside Lightship, Niantic is now pushing Campfire, “a new social app that helps Niantic Explorers discover new people, places and experiences around them.”

- Finally, TikTok’s up-and-coming Effect House and startups like Blippar, Zappar, and VuForia further broaden the range of options, enabling developers to choose their preferred platform depending on their own priorities, whether it be reach, ease of use, or specific features.

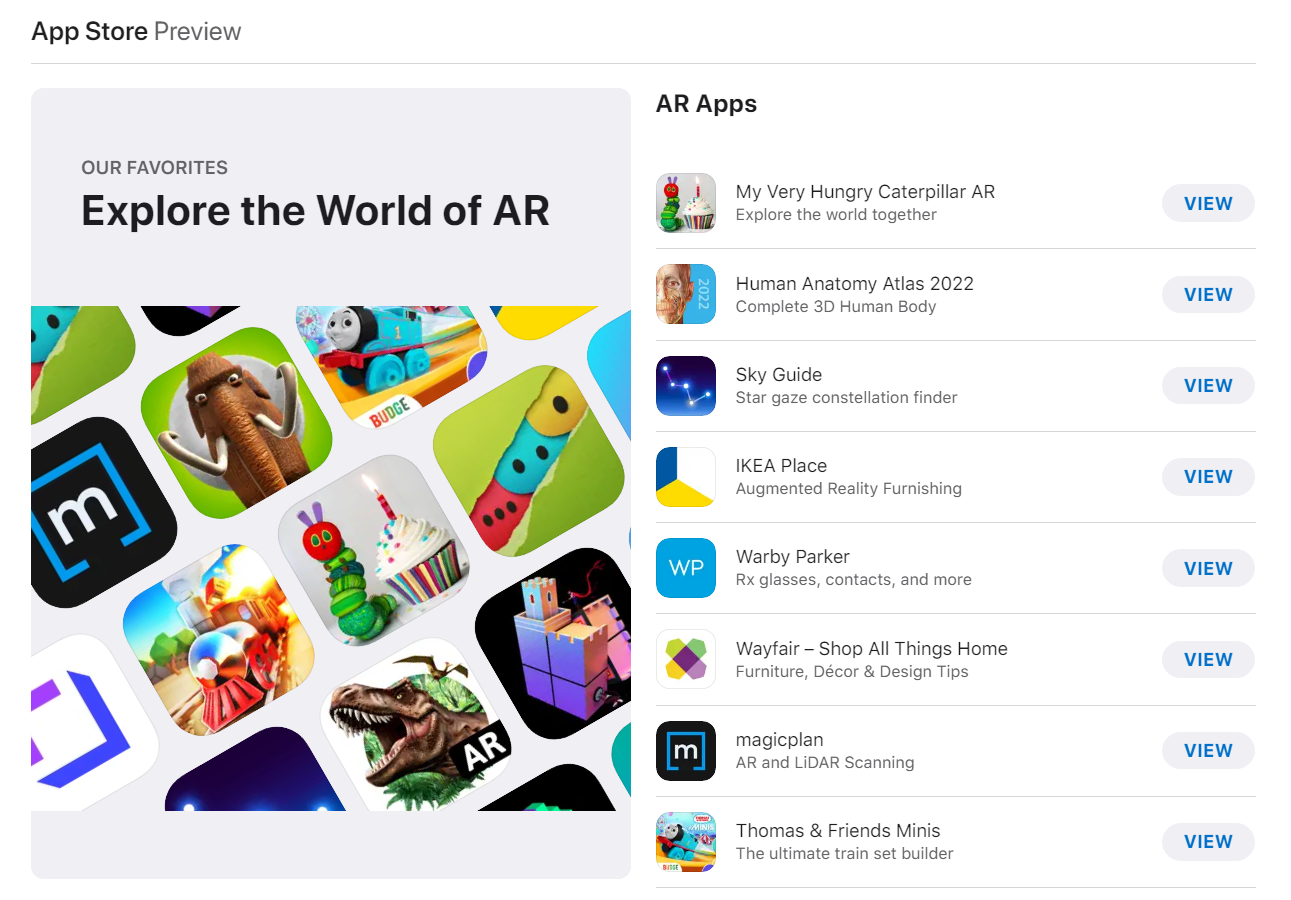

All these efforts have been a boon for the application layer, as developers leveraged these newfound capabilities to wow consumers — in June, Apple’s Tim Cook teased an impressive 14,000 AR apps on the App Store. Retail was among the first industries to dive in in 2017 with IKEA Place, followed by numerous household names, with Sephora, Warby Parker, Adidas, and Nike all using the technology for virtual try-ons. New use cases continue to appear, including wellness: TRIPP, a mindfulness-focused immersive platform, recently expanded from VR and mobile to AR, too. (N.B. TRIPP is a BITKRAFT portfolio company.)

On the entertainment front, Pokémon Go remains unassailable — the game hit $6B in lifetime revenue in June — but others like SpotX (recently acquired by Niantic) and Resolution Games (another BITKRAFT portfolio company) are now tackling the segment too. Still, success is anything but a given: even Niantic has been struggling to replicate the success of Pokémon Go, and had to shut down Harry Potter: Wizards Unite after the game failed to take off. As with gaming at large, even the most powerful IP won’t make up for lackluster execution.